Climate Scenario Analysis - Looking to the Long term for Investors

Written by Aberdeen Standard Investments

Climate change is one of the biggest issues facing the world today. Many governments, countries and industries have recognised the threat and are taking measures to try to counter it. Much depends on their success or failure.

As asset managers, however, our primary interest is in the investment implications. Our recent White Paper uses a scenario-based approach to examining the subject in depth.

Below, we take a brief look at how the output from our analysis has influenced our long-term forecasts for asset classes.

When we decide how to construct portfolios over the long-term, we use a structured framework. We call this strategic asset allocation (SAA). When we carry out SAA, we look at what we expect a large variety of asset classes to do over given periods. Then we consider how to combine them into portfolios in order to meet investors’ long-term objectives. Our understanding of the likely impacts of climate change means it is imperative for us to consider how it might affect portfolio performance.

Building on our existing economic scenarios

Generally, we base our asset-class forecasts on developing a range of economic scenarios. For each of these, we make a set of different assumptions. These are likely to include prevailing rates of economic growth, inflation and interest. We then consider the probability of each scenario. From there we decide our probability-weighted mean ‘expected’ returns.

These are behind the SAA advice that we give to our clients. Since scenarios have long played an active role in our process, it is natural for us to use them when we consider the long-term effects of climate change on investment returns. Our approach is very similar to the one we use for other aspects of SAA, and we can in fact combine the two effectively.

What are the financial effects of climate change?

The goal of the Paris Agreement is to “limit global warming to well below 2, preferably to 1.5 degrees Celsius, compared to pre-industrial levels”. Based on our climate scenario analysis, we think it’s likely that the world will fall short of the “well below 2 degrees” goal.

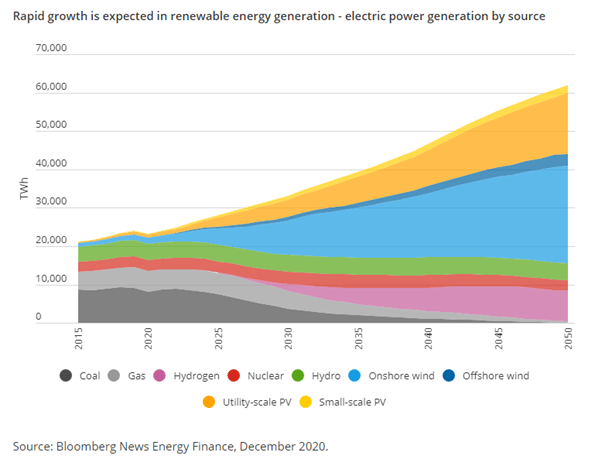

However, our central scenarios suggest that a major energy transition is underway. Both stronger government policies and improving low-carbon technologies suggest that this will prove durable. It seems that significant change is almost inevitable. And there will be implications for a number of business sectors.

Rapid growth is expected in renewable energy generation – electric power generation by source

This could translate into high earnings growth for the companies driving the transition in these areas. Conversely, demand for coal, eventually oil and potentially gas will start to fall, suggesting low or negative growth rates in earnings for these sectors.

When forecasting long-term equity returns in SAA, we use a simple discounted-cash-flow (DCF) approach of the kind used widely by fundamental equity investors. In this model, long-term investment returns are highly sensitive to earnings growth rates. In the simplest DCF equation [1], all else equal, the higher the earnings growth rate, the higher the company value. If the winners of the climate transition have the kind of growth rates implied by the charts above, they will have high justified valuations – particularly if interest rates remain structurally low [2].

Scenarios are invaluable modelling tools

High growth rates for renewable energy and electric vehicles are likely but not guaranteed. If governments were to backslide on their stated climate ambitions, growth would be significantly lower. Similarly, interest rates may not remain at today’s historically low levels. For example, they may rise in a more sustained inflationary environment – reducing valuations, particularly for high-growth stocks.

Climate scenarios are invaluable tools that allow us to model this uncertainty. We think it is important to be able to assess the impact on returns across a range of different climate scenarios and to regularly retest assumptions on returns as market prices and climate policies shift. This is what our climate tools aim to enable.

The effect on our forecasts

As we show in our White Paper, our 15 climate-scenarios provide us with a distribution of potential earnings growth and valuation outcomes for individual companies and aggregate indices.

Aggregate Indices

In short, when we take the average impact of our climate scenarios we find that the overall effect on equity market indices such as the MSCI World is very small. The climate ‘winners’ are offset by the climate ‘losers’ and on average this impact is small. Between and within individual sectors, it is much larger – fossil fuel companies lose, renewables and electric vehicles win.

The story is the same for corporate bond indices, though here time is more of a factor. The biggest impact of the climate transition on credit risk will be in the 2030s and beyond – for example, as oil demand falls. Bonds that will be redeemed within 10 years are little affected by this risk. It is only the small minority of very long-dated bonds (e.g. an oil company’s 20-year bond) that are severely affected.

From an SAA perspective, this means that climate scenarios change our standard forecasts for equity and bond indices only a little.

Sector & Company Level

The story is very different across and within individual sectors. Sector valuation impacts are over 10% in some sectors (e.g. oil & gas and utilities), meaning reduced returns for investors in these sectors.

The impact is even more pronounced when looking at individual companies. For example, our valuation estimates for some companies are reduced by 50% when factoring in climate change. That is under our mean scenario. Under more extreme scenarios, which are possible, if the pace of climate action is too slow, the impact could be even larger. These impacts are big enough to make a substantial difference to SAA forecasts, and to subsequent asset-allocation decisions.

This creates significant potential for long-term investors to focus strategically on shifting allocations to investment themes and sectors that are particularly strong at mitigating climate risk or exploiting new climate-related opportunities.

End

References

[1] 3 P = D/(r-g) where P is fair-value price, D is dividend in year 1, r is discount rate (comprising the risk-free interest rate and the equity risk premium) and g is the earnings-growth rate.

[2] Low interest rates mean lower discount rates in the DCF equation.

Important Information:

Capital at risk.

Investment involves risk. The value of investments, and the income from them, can go down as well as up and an investor may get back less than the amount invested. Past performance is not a guide to future results.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as of date of publication and may change without notice.

Issued by Aberdeen Standard Investments Ireland Limited. Registered in Republic of Ireland (Company No.621721) at 2-4 Merrion Row, Dublin D02 WP23. Regulated by the Central Bank of Ireland .